Climate and Sustainability Regulations: 2024 End-of-Year Review

Climate and Sustainability Regulations: 2024 End-of-Year Review

2024 was an active year for environmental, social and governance (ESG) regulations, voluntary reporting standards, and stakeholder policies. While the incoming Trump administration is expected to halt federal sustainability reporting regulations for the next four years, 2024 saw several significant state and international regulatory developments that will impact US and other companies in 2025. In addition to numerous significant pending regulations, 2025 will see many companies busily preparing for initial disclosures under existing regulations, such as the California climate statutes and the European Union’s Corporate Sustainability Reporting Directive (CSRD).

This client alert provides an overview of the current state of key climate and sustainability regulations, as well as significant stakeholder developments as of the end of 2024. It also highlights critical areas of focus for the year ahead.

US takeaways of note

Federal and state legislation are increasingly diverging in their approaches to sustainability regulation – in particular, sustainability reporting. Specific highlights include:

1. Securities and Exchange Commission (SEC) climate disclosure rules fail to launch

The long-awaited SEC climate rules, adopted in March 2024, were voluntarily stayed by the SEC in April pending resolution of ongoing federal litigation consolidated in the US Court of Appeals for the Eighth Circuit. While the specific procedural approach of the incoming Trump administration remains to be seen, the SEC climate rules are certainly not expected to receive support. As a result, companies do not expect to report under SEC climate rules in the near future. With SEC climate or other ESG reporting mandates no longer anticipated, many companies will nonetheless find themselves subject to ongoing stakeholder and regulatory pressure to report on climate and other sustainability topics, including upcoming reporting under the EU’s CSRD and California climate statutes.

2. Sustainability-focused legislation at the US state level

As discussed in this September 2024 client alert, climate reporting continues to be a focus of state-level legislation, primarily led by California, but with similar bills having been proposed and debated in Illinois, New York and Washington. On September 27, 2024, California Gov. Gavin Newsom signed Senate Bill 219 into law, with implications for the California Climate Corporate Data Accountability Act (SB 253) and the Climate-Related Financial Risk Act (SB 261). The most significant result of SB 219 is that the California Air Resources Board (CARB) will have an extra six months (until July 1, 2025) to issue implementing regulations under SB 253. Further, recent legal challenges to these laws have been unsuccessful.

More recently, on December 5, CARB put out an enforcement notice providing leniency in the first year of reporting. In particular, CARB will allow companies to report Scopes 1 and 2 emissions in 2026 based on existing data and data collection processes, rather than needing to update based on CARB guidance. CARB also will not take enforcement actions against companies that report incomplete data in 2026, as long as companies make a good-faith effort to retain the relevant data. In addition, on December 16, CARB announced the solicitation of public comment in response to 13 questions related to SBs 253 and 261, with a comment deadline of February 14, 2025. Topics include the definition of “doing business in California,” whether CARB should require greater standardization in areas where the Greenhouse Gas (GHG) Protocol allows flexibility, standards for third-party assurance providers, integration of external reporting standards, and the relevant time frame for information included in SB 261 reporting. Although CARB’s solicitation of public comment includes limited questions related to SB 261, unlike SB 253, CARB is not required to pass rules implementing SB 261 and has not issued guidance to date. As a result, there remains ongoing uncertainty among companies as to the degree of alignment regarding disclosure under SB 261 and all aspects of the Task Force on Climate-Related Financial Disclosures (TCFD) standards.

Although federal sustainability reporting regulations generally did not advance in 2024 and have dim prospects for the next four years, ESG-related obligations are not limited to the climate. The US Department of Homeland Security continues to increase the number of entities on the Uyghur Forced Labor Prevention Act (UFLPA) entity list, expanding the number of goods presumed to be derived from forced labor and thus prohibited from import into the US. UFLPA enforcement under the next administration is expected to be significantly influenced by broader US government trade policy. Canada also appears to be following suit, having recently announced its intention to introduce a new supply chain due diligence regime.

3. Developments in US anti-greenwashing laws

While California’s Voluntary Carbon Market Disclosure Act (Assembly Bill 1305) came into effect on January 1, 2024, at the federal level, we are still waiting on Federal Trade Commission (FTC) revisions to the Green Guides. In April 2023, the FTC requested public comment on proposed revisions to the Green Guides – including new guidance on climate-related claims, such as “carbon neutral,” “net zero” and claims regarding recyclability. Various attempts to amend the bill have stalled (for more, see Cooley’s September 2024 update). Despite the quiet disbanding of the SEC ESG task force in mid-2024, the SEC has continued to focus on misleading sustainability claims in its enforcement actions, recently imposing fines of $1.5 million and $17.5 million for, respectively, alleged inaccuracies in recyclability statements made in a company’s annual reports and misleading statements about supposed investment considerations. In addition to SEC enforcement actions, private litigation has continued to proliferate regarding greenwashing claims, as has enforcement at the state level – including lawsuits brought by California and Ford County, Kansas, regarding plastics recycling – in 2024.

4. Climate and sustainability remain ongoing activist focus areas

Environmental and social proposals continued to be submitted in robust numbers in 2024, with 197 environmental proposals received (198 in 2023) and 416 social proposals received (421 in 2023). While the number of traditional environmental and social proposals had been trending downward, a higher number of anti-ESG proposals submitted in 2024 kept overall totals in line with 2023 (see our 2024 Shareholder Proposal Highlights). While the 2024 proxy season saw an approximate 30% rebound in no-action letter requests and robust success rates of nearly 70%, with the incoming Trump administration, many companies are hopeful that they will receive an even more sympathetic reception – particularly on environmental and social proposals, where companies have struggled to receive Rule 14a-8(i)(7) micromanagement relief in recent years.

Governance proposals received more support in 2024, unlike social and environmental proposals, with average shareholder support of 34%, compared to 29% in 2023. Environmental (18% support, compared to 21% in 2023) and social (15% support, compared to 18% in 2023) proposals both recorded lower support than in the previous season. Notably, many large institutional investors had low support for environmental and social proposals. For example, Vanguard did not support any environmental proposals in 2024, while BlackRock supported only four. However, the voting patterns of large institutional investors do not necessarily indicate a departure from their prior support for companies’ incorporation of environmental and social stewardship. As BlackRock noted in its 2024 Global Voting Spotlight, “we observed enhanced disclosure around how companies are managing material climate-related risks,” thus finding that, in many instances, companies have already undertaken substantive action related to such proposals. Proxy advisor and institutional investor policies in 2023 and 2024 have not introduced any major changes with regard to environmental and social proposals and have only introduced relatively minor refinements, such as BlackRock updating its policy to include eventual alignment around International Sustainability Standards Board (ISSB) standards.

International takeaways of note

Sustainability reporting

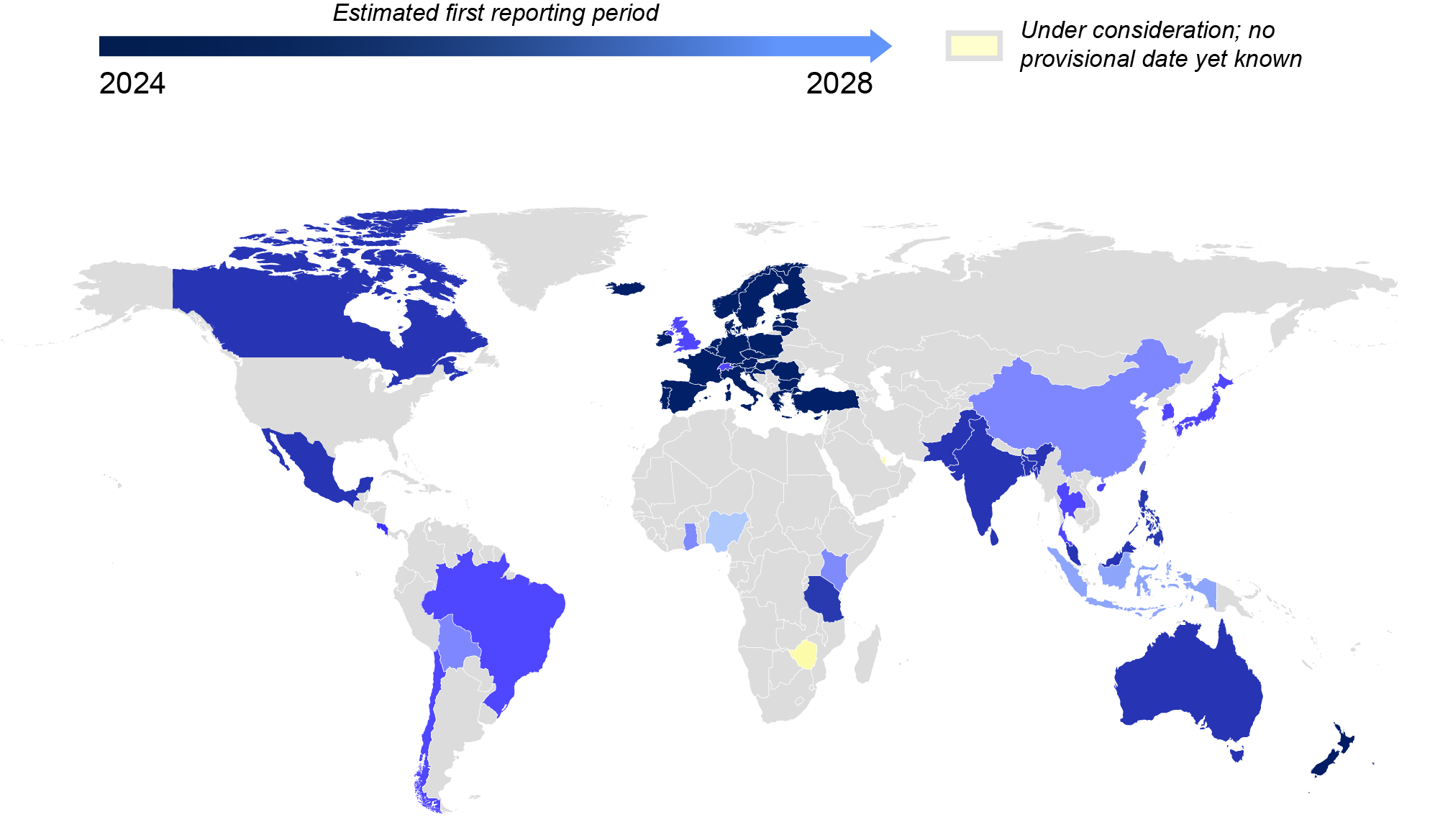

Mandatory sustainability disclosures are becoming the global norm with broad convergence around two major frameworks – the ISSB’s standards (IFRS S1 and S2) and the EU’s CSRD and accompanying European Sustainability Reporting Standards (ESRS).

A November 12, 2024, publication from the International Financial Reporting Standards (IFRS) Foundation reported that 30 jurisdictions representing more than 40% of global market capitalization have already decided to use or are taking steps to introduce ISSB standards into their regulatory frameworks, with many countries seeking full alignment. Most recently, Qatar launched a consultation on ISSB adoption.

The international ESG reporting landscape is currently a patchwork of upcoming mandatory and voluntary disclosures, with jurisdictions taking different approaches to the phase-in (often grace periods for Scope 3 emissions disclosures) and scope of obligations.

ISSB standards (or close local equivalent) implementation

The EU remains at the forefront of sustainability reporting. Key headlines include:

1. Companies start to align voluntary reporting in preparation for the EU’s CSRD

The first wave of companies required to report under the CSRD – mostly companies listed on an EU regulated market – will need to report on the ESRS for their financial years starting in 2024. This means we will start to see the first formal CSRD reports being published during 2025. To prepare for CSRD reporting, some companies are already starting to publish “CSRD-style” reports. We analyzed 20 of these early CSRD-style reports in August 2024. While certain EU member states missed the deadline for implementing the CSRD into their national laws, this is not wholly unusual, and the European Commission has taken steps to try to make sure the implementation process is completed on time.

2. As the deadline for CSRD compliance nears, further guidance is published to support preparation

On November 13, 2024, the European Commission adopted a set of FAQs to further support companies with the implementation of the CSRD. Other publications include the European Securities and Markets Authority (ESMA) Final Report on the Guidelines on Enforcement of Sustainability Information and public statement on the first application of the ESRS, which highlight key areas of focus for companies when preparing sustainability reports – in particular, the need for robust governance arrangements and internal controls.

The European Financial Reporting Advisory Group (EFRAG) also published nonbinding implementation guidance on materiality assessments, value chains and data points, as well as ISSB interoperability guidance and early drafts of its climate transition plan guidance. Rolling updates to EFRAG’s Q&As on the ESRS continue to be published (see explanations from January to November 2024 and December 2024), including a mapping of sustainability matters against ESRS disclosures. On September 10, 2024, EFRAG endorsed the United Nations’ Sustainable Development Performance Indicators as a robust tool for measuring ESG factors in accordance with the CSRD.

3. Preliminary drafts of sustainability disclosure standards for non-EU companies in scope of CSRD published

These standards will start to apply to many non-EU parent companies from financial years starting on or after January 1, 2028. While less onerous than the ESRS for EU companies, they will nevertheless represent a step up for most multinationals as compared to current voluntary reports. These drafts will be further discussed and developed during 2025.

4. International Auditing and Assurance Standards Board approves assurance standard on sustainability information: ISSA 5000

Published in November 2024, ISSA 5000 is intended to serve as a stand-alone standard suitable for any sustainability assurance engagements and is applicable to sustainability information reported across any sustainability topic and prepared under multiple frameworks. It is expected that the EU will adopt this standard as a reference point for CSRD assurance. Until then, the EU’s Committee of European Audit Oversight Bodies has published nonbinding guidelines on limited assurance.

However, sustainability reporting developments are not limited to the EU. Internationally, other key developments include:

- Australia’s Treasury Laws Amendment (Financial Market Infrastructure and Other Measures) Act 2024 introduced climate-related disclosures aligned with the ISSB for certain large companies. Effective from September 18, 2024, the requirements started to apply to the largest companies from January 1, 2025, with the first sustainability reports due in 2026. Similarly pressing are the new Mexican sustainability standards, which apply to certain private companies, including subsidiaries of foreign multinationals, from financial years starting on or after January 1, 2025.

- Other countries continue to press ahead with drafts of their own national sustainability reporting standards. The Canadian Sustainability Standards Board published the Canadian Sustainability Disclosure Standards (CSDS) on December 18, 2024. While largely aligned with the ISSB standards, the CSDS extend certain transition reliefs giving companies extra time to prepare disclosures, such as those on Scope 3 GHG emissions. On December 17, 2024, China also released a trial version of the “Sustainability Disclosure Standards for Enterprises – Basic Standards,” with accompanying Q&As suggesting that these standards will be finalized by 2027, and that China intends to expand sustainability reporting from listed companies to private companies. Additionally, companies in Singapore are still waiting on anticipated amendments that will introduce sustainability reporting for private companies, with drafts now expected in Q1 2025.

- The UK government has reiterated its ambition to adopt UK Sustainability Reporting Standards (SRS) based closely on the ISSB standards. The UK government aims to consult on the exposure drafts in Q1 2025. To date, only minor amendments to the ISSB standards have been proposed by the UK’s Technical Advisory Committee in its recommendations to the UK government. Once endorsed and subject to consultation, the Financial Conduct Authority (FCA) is expected to introduce requirements for UK-listed companies to report sustainability-related information to their investors. The UK government also is considering mandatory sustainability reporting for “economically significant companies.” Depending on the outcomes of these processes, the UK SRS could be effective for accounting periods beginning on or after January 1, 2026. The UK FCA also recently completed a consultation on proposals for new prospectus rules that govern public offers and admissions to trading. As proposed, the new rules would require, where necessary, additional disclosures on climate-related risks and opportunities. The FCA plans to finalize the new rules by mid-2025, after which the rules will come into force following a transition period.

- Switzerland’s recent proposals appear more ambitious. On December 6, 2024, the Swiss government launched a consultation on amendments to the Climate Disclosure Ordinance (open until March 21, 2025). Under the proposal, certain companies would be required to disclose 2050-aligned, net-zero transition plans. The proposal also permits companies to satisfy their climate-reporting obligations where they are already reporting in compliance with an internationally recognized standard, such as the ISSB standards or the ESRS.

- Increasing investor expectations that companies’ financial and nonfinancial reporting reflect climate risks. On July 12, 2024, the International Corporate Governance Network released a report outlining investors’ expectations for sustainability disclosures and the quality of external assurance, emphasizing that these reports should be prepared with the same rigor and ethics as financial statements. Meeting this growing global demand for more detailed and globally comparable climate reporting, the IFRS published implementation guidance for companies: Voluntarily applying ISSB Standards – A guide for preparers (published on September 25, 2024) and a guide to help companies identify material sustainability-related risks and opportunities (published on November 19, 2024). Further responsive to investor concerns about insufficient or inconsistent climate data in company financial statements, on July 31, 2024, the International Accounting Standards Board, in collaboration with ISSB, published draft illustrations of how companies should report on the effects of climate-related and other uncertainties in their financial statements.

5. Rise of the ‘global reporting passport’

With the growing number of sustainability reporting standards joining existing voluntary frameworks, 2024 has seen a focus on interoperability and alignment, leading to further convergence of commonly used frameworks. As standards converge, companies will be able to prepare their reports once and use the data points to satisfy multiple global reporting obligations.

- Interoperability with the ESRS – Guidance on the interoperability among the ISSB-ESRS, the Taskforce on Nature-related Financial Disclosures-ESRS, and GHG emissions reporting under ISSB-GRI have been published to help companies navigate outstanding differences. A new GRI-ESRS linkage service also was launched to give Global Reporting Initiative (GRI) reporters feedback on how existing reporting areas of overlap between the ISSB and ESRS can be expected as the ISSB continues to develop sustainability reporting standards on biodiversity, ecosystems and ecosystem services, and human capital. Further detail on next steps is expected in the first half of 2025.

- CDP has fully aligned its 2024 corporate questionnaire with the IFRS S2 (ISSB) climate standard, and on November 12, 2024, it announced extensive interoperability with ESRS (E1), meaning CDP-disclosing companies will be well prepared for climate disclosures required by the CSRD. A comprehensive mapping of the two frameworks is due to be published early next year, ahead of the 2025 CDP disclosure cycle.

- Sustainability Accounting Standards Board (SASB) standards are likely to be revised to ensure consistency with new sustainability standards, with the ISSB discussing development of targeted amendments.

- Convergence is not limited to existing standards. Following the September 2024 launch of the new global Taskforce on Inequality and Social-related Financial Disclosures (which is developing disclosure recommendations to support companies and financial institutions in more effectively disclosing impacts, dependencies, risks and opportunities related to social issues), standards bodies, such as the EU’s EFRAG, have already entered into cooperation agreements to ensure alignment on social-related financial disclosures.

ESG ratings providers

Mandatory rules for ESG ratings providers on the horizon

A common criticism of ESG ratings agencies is the lack of correlation between one rating agency’s assessment of a company’s activities compared to those of its competitors, leading to rating-shopping. Since the International Organization for Securities Commissions (IOSCO) published its recommendations to improve the transparency of ESG ratings in November 2021, several jurisdictions have taken steps to increase oversight over ratings providers.

UK government publishes draft legislation to regulate ESG ratings providers

On November 14, 2024, the UK government published draft legislation to regulate ESG ratings providers, which requires rating providers to obtain authorization from the UK FCA and comply with a new regulatory regime (expected in 2025). The new rules are expected to increase transparency and the coherence of ratings in line with IOSCO’s recommendations.

EU remains one step ahead

The EU adopted its own ESG Ratings Transparency Regulation on November 19, 2024, which will start to apply on July 2, 2026. ESG ratings providers will need to be authorized by ESMA to avoid conflicts of interest, along with complying with new transparency requirements – e.g., disclosing their methodology, models and key ratings assumptions. With some exceptions, the new rules require separate environmental, social and governance ratings to be provided rather than a single aggregated rating. Infringement penalties can be up to 10% of global revenue.

Sustainable finance

Increased EU Sustainable Finance Disclosure Regime (SFDR) enforcement anticipated

According to ESMA’s 2025 Annual Work Programme, in 2025, it will be focusing on the implementation of the EU’s sustainable finance frameworks, combating greenwashing and promoting transparency in sustainable investments. Already, fines for noncompliant funds have been issued – most recently by the Luxembourg authorities.

Keep an eye out for potentially significant changes to the EU’s SFDR

The European Supervisory Authorities’ opinion (June 2024), alongside ESMA’s opinion (July 2024), recommended the European Commission amend the current SFDR legislation to reduce greenwashing risks. Proposed changes included a requirement that all financial products disclose some minimum basic sustainability information, and that the EU taxonomy should become the sole reference point for the assessment of sustainability – meaning managers may be required to apply a more science-based, as opposed to principle-based, measurement for an investment to qualify as sustainable. In the meantime, the updated FAQs published in July 2024 on the practical application of the SFDR, guidelines on ESG funds’ names and related Q&As published December 13, 2024, and FAQs on the application of the EU taxonomy published November 29, 2024, should provide some clarity to investors and companies in scope.

Interoperability is an increasing focus

On November 14, 2024, the International Platform on Sustainable Finance published a Multi-Jurisdiction Common Ground Taxonomy, setting out a comparison of sustainable taxonomies in the EU, China and Singapore to further interoperability efforts among domestic green taxonomies and enabling market participants to assess what could be considered “green” in each of the three jurisdictions. In November 2024, the UK launched a consultation on the development of its own green taxonomy (closing in February 2025), noting interoperability as a particularly important factor for any future requirements.

UK FCA partially delayed implementation of its Sustainable Fund Labelling Rules to April 2, 2025

These rules will restrict the use of certain sustainability-related terms, such as “ESG” or “sustainable,” in product names and marketing materials (see ESG 4.3.2R to ESG 4.3.8R of the ESG sourcebook). While the labeling rules apply from December 2, 2024, the FCA has provided temporary relief until April 2, 2025, for certain funds, provided specific conditions are met – including that an application for approval of amended disclosures was made by October 1, 2024. Meanwhile, the outcome of the FCA’s consultation on whether to extend these labeling rules to portfolio management services, also proposed to be effective from December 2, 2024, is not yet known. The FCA’s anti-greenwashing rule and related guidance applicable to all FCA-authorized firms as of May 31, 2024, continue unimpacted by this partial delay.

Greenwashing

Anti-greenwashing rules continue to be implemented and enforced globally

Earlier this year, the UK Competition and Markets Authority (CMA) took action against a range of companies for misleading sustainability claims (see Cooley’s May 2024 summary). Since then, the CMA has received new enforcement powers under the UK’s new Digital Markets, Competition and Consumers Act 2024, giving it the ability to impose fines of up to 10% of global turnover for noncompliance. The CMA’s annual plan for 2024 – 2025 made clear that environmental sustainability remains a policy and enforcement priority, and recently released practical guidance for business leaves little room for doubt as to what companies should avoid.

Increased scrutiny also can be seen in Australia, with its securities commission reporting to have made 47 regulatory interventions to address greenwashing misconduct during the 15-month period up to June 30, 2024, and which recently issued a penalty of AUS$12.9 million to an investment firm for making misleading ESG claims. Further, Canada has amended its Competition Act to directly target greenwashing rather than assessing such claims under false or misleading claims regulations. Broadly speaking, the amendments require that representations that a product or business activity can protect or restore the environment must be based on adequate testing pursuant to an “internationally recognized methodology” before public dissemination.

Strict new EU anti-greenwashing rules were adopted in 2024

The Empowering Consumers for the Green Transition Directive, set to apply from September 27, 2026, updates existing consumer laws and will ban most generic environmental claims – such as “sustainable” and “green,” and any claims that a product or service has a neutral, reduced or positive impact on the environment, when those claims are based on GHG emissions offsets. The corresponding Green Claims Directive, requiring sustainability claims to be substantiated, is still under development.

Third-party verification and net-zero standards are crucial for mitigating the risks of greenwashing. Reflecting the increasing demand for verifiability and comparability, further notable developments include:

- The EU’s adoption of legislation establishing an EU-level certification framework for permanent carbon removals, carbon farming and carbon storage products (November 19, 2024). While this framework is voluntary, it is aimed at creating a certification system to quantify, monitor and verify carbon removals to counter greenwashing. Under the framework, carbon removal activities will need to achieve a quantified net carbon removal or soil emissions reduction benefit, go beyond statutory requirements, aim to ensure long-term carbon storage and do no significant harm. Activities seeking certification will need to be independently verified.

- The Science Based Targets initiative (SBTi) delayed its decision on whether offsets can play a greater role in emissions reduction targets finding “clear risks” to using carbon credits to offset emissions. Having previously indicated in April 2024 that it could relax its rules currently limiting the use of carbon offsets in achieving absolute emissions reductions, SBTi’s findings, published in July 2024 (and arising from its review of 111 third-party studies on performance of carbon credits), concluded that “various types of carbon credits are ineffective in delivering their intended mitigation outcome,” and that more research was needed. Stopping short of providing SBTi’s likely final position on the role of carbon offsets, greater clarity is expected with the publication of Corporate Net-Zero Standard 2.0, projected for release in Q4 2025.

- The International Organization for Standardization is preparing to launch its own global net-zero standard at the 2025 UN Climate Change Conference (UNFCCC COP 30). This new standard hopes to offer companies clear, independently verified guidelines for achieving their net-zero targets, providing a globally consistent approach to climate action across industries and regions.

In case you missed it – beyond ESG disclosures

Between 2019 and 2024, the EU published 108 pieces of legislation under the European Green Deal. A significant proportion of these have been adopted with implications for EU and non-EU companies of all types. While the most prominent of these are the EU’s CSRD and Corporate Sustainability Due Diligence Directive (see our April 2024 client alert and the European Commission’s recently published FAQs), for companies, many of the new sustainability requirements for product design, manufacture and end of life are much more pressing. Conversations on potential changes under the proposed “omnibus” simplification package – allegedly aimed at reducing reporting burdens for companies – have so far neglected to recognize that many of the disclosures also are required under other industry-specific legislation. Greater clarity on what form this “simplification package” will take is expected in February 2025. At this stage, it is not expected that the publication of the “simplification package” will lead to a delay in CSRD reporting deadlines for businesses.

Check out Cooley’s Productwise blog for more product-related insights on sustainability regulations – many of which have looming compliance deadlines for products sold in the EU and their supply chains – including the EU’s Batteries Regulation (certain provisions already in effect), Deforestation Regulation (applying from December 30, 2025), and the recent Forced Labour Regulation (applying from December 4, 2027).

대화 참여하기